EMPLOYEES’ OLD-AGE BENEFITS BILL, 2026

A Bill

“to repeal and re-enact the Law relating to the old-age benefits for the persons employed in industrial, commercial, agricultural and other organizations or otherwise.”

WHEREAS it is expedient to repeal and re-enact the law relating to old-age benefits for the persons employed in industrial, commercial,

agricultural and other organisations or otherwise and matters connected therewith:

It is hereby enacted as follows: –

CHAPTER – I PRELIMINARY

- Short Title, Extent, Commencement and Application. —

(1) This Act may be called the Employees’ Old-Age Benefits Act, 2026.

(2) It extends to the whole of Pakistan.

(3) It shall come into force at once.

(4) It applies to:

(a) every industry or establishment:

(i) wherein five or more persons are employed by the employer, directly or through any other person, whether on behalf of himself or any other person, or were so employed on any day during the preceding twelve months, and shall continue to apply to every such industry or establishment even if the number of persons employed therein is, at any time after this Act becomes applicable to it, reduced to less than five;

(ii) wherein less than five persons are employed if such industry or establishment voluntarily applies for the application of this Act, and this Act shall apply to such industry or establishment from the date of submission of an application by such industry or establishment;

(iii) which the Government may, by notification in the official Gazette, specify in this behalf;

(b) the self-employed persons, overseas Pakistani workers, including emigrant workers, the informal workers including but not limited to domestic workers, home-based workers, agricultural workers, and street vendors, homemakers including housewives, and all other Pakistani citizens aged between 16 and 58 years who voluntarily apply for the application of this Act, as prescribed, and this Act shall apply to them from the date of submission of such application.

- Definitions. — In this Act, unless the context otherwise requires, –

- “administrative ministry” means the Ministry responsible for the administration of the Employees Old Age Benefits Act, 2026 and the Employees Old Age Benefits Institution;

- “authorised officer” means an official of the Institution, duly authorised by a certificate as per regulations;

- “benefits” mean old-age pension, invalidity pension, survivor’s pension, old-age grant and such other benefits notified by the Government;

- “Board” means the Board of Trustees constituted under section 7;

- “care credit” means a period of deemed insurable employment and deemed contribution credited to an insured person’s contribution record under section 33, financed in the prescribed manner;

- “care period” means a period during which an insured person provides unpaid primary care to:

(i) a child from birth until such age as may be prescribed; or

(ii) a person with severe disability; or

(iii) an elderly person requiring intensive care, as may be prescribed;

- “Contribution” means the sum of money payable to the Institution by the employer, the insured person or by the Government under the provisions of this Act.

- “Contribution base” means the amount of wages on which contributions shall be computed by the employers and the insured persons, provided that the contribution base shall not be less than the minimum wage for unskilled workers, as notified by the Islamabad Capital Territory Administration;

- “employee” means any person employed, whether directly or through any other person, for wages or otherwise, to do any skilled or unskilled, supervisory, clerical, professional, intellectual, manual or other work in, or in connection with the affairs of, an industry or establishment, under a contract of service or apprenticeship, whether written or oral, express or implied, and includes such person when laid off as well as any person or class of persons which the Government may specify by notification in the official Gazette:

Provided that a director of a limited company or of a corporation set up under any law shall not be treated as an employee under this Act, irrespective of his or her wages or emoluments.

- “employer” means any person, whether natural or legal, that employs an employee, and includes-

(a) in the case of an individual, an heir, successor, administrator or assign;

(b) a person who has ultimate control over the affairs of an industry or establishment, or where the affairs of an industry or establishment are entrusted to any other person (whether called a managing agent, managing director, manager, superintendent, secretary or by any other name), such other person; and

(c) where any work or undertaking is carried on by or on behalf of the State, the contractor or licensee, executing or carrying on such work or undertaking;

- “employment injury” means a personal injury to an insured person caused by an accident, or by such occupational disease as may be specified in the regulations, arising out of and in the course of employment;

- “establishment” means an organisation, whether industrial, commercial, agricultural or otherwise, and includes. –

(i) any, business, trade, profession, service, calling, or any other economic activity being carried out for the purpose of profit or gain or otherwise, including charitable organisations of whatsoever nature and further includes any establishment which the Government may notify;

(ii) a construction industry as defined in the West Pakistan Industrial and Commercial Employment (Standing Orders) Ordinance, 1968 (West Pakistan Ordinance No. VI of 1968) or any other relevant law for the time being in force;

(iii) a factory as defined in the Factories Act, 1934 (XXV of 1934) or any other relevant law for the time being in force;

(iv) a mine as defined in the Mines Act, 1923(IV of 1923) or any other relevant law for the time being in force;

(v) a road transport service as defined in the Road Transport Workers Ordinance, 1961 (XXVIII of 1961) or any other relevant law for the time being in force; and

(vi) any class of industries or establishments which the Government may, by notification in the official Gazette, declare to be industry or establishments for the purposes of this Act:

Provided that societies registered under the Societies Registration Act, 1860 (Act XXI of 1860), or any other relevant law for the time being in force, may opt for the scheme voluntarily in respect of their members, who shall be treated as insured persons for the purpose of this Act, including payment of contribution and advancement of benefits.

- “fund” means the Employees’ Old-Age Benefits Fund set up under section 21;

- “Government” means the Federal Government of Pakistan;

- “homemaker” means the family members dependent on and living in the house of the person paying the contributions in respect of them, including but not limited to spouse, children, parents, and siblings;

- “industry” means any service, business, trade, undertaking, manufacture or calling of employers, and includes any calling, service, employment, handicraft, industrial occupation or avocation of workers;

- “institution” means the Employees’ Old-Age Benefits Institution established or nominated under section 4;

- “insured person” means an employee and a self-employed person for whom contributions are or were paid;

- “insurable employment” means employment of a person in respect of which contributions are paid under the Act by the employer and the insured person, provided that for the category of persons specified in section 1(4)(b), it refers to the period for which contributions are paid by such persons;

- “invalidity” means a condition, other than that caused by an employment injury, as a result of which an insured person is incapacitated to such an extent as to earn from his or her usual or other occupation more than one-third of the normal rates of earning in usual occupation;

- “member” means a member of the Board;

- “mine worker” means a person employed in a mine as defined in section 3(f) of the Mines Act, 1923 or any other relevant law for the time being in force;

- “minimum pension” means the minimum pension duly notified by the Board in the official gazette, which shall not be less than 40% of the contribution base;

- “overseas Pakistani worker” means a citizen of Pakistan or holder of NICOP/POC lawfully employed or self-employed outside Pakistan;

- “prescribed” means prescribed by rules or regulations made under this Act;

- “regulations” means regulations made under this Act;

- “rules” means rules made under this Act;

- “self-employed” means an individual who works or provides services in person for gain or reward, other than under a contract of employment, including an agricultural worker, a home-based worker, a digital labour platform worker, whether engaged in location-based work or online freelance work, a street vendor, a domestic worker, an informal economy worker, and includes any other person which the Government may, by notification in the official Gazette, specify in this behalf;

- “special package” means a special package offered to insured persons who want to have an enhanced pension on payment of enhanced contributions, in the prescribed manner;

- “wages” means all remunerations capable of being expressed in terms of money, which would, if the terms of contract of employment, express or implied, were fulfilled, be payable to a person employed in respect of his or her employment or of work done in such employment, but does not include:

- any contribution paid by the employer in respect of such person under any scheme of social insurance or to a pension fund or provident fund;

- any travelling allowance or the value of any travelling concession;

- any sum paid to such person to defray special expenses incurred by him in respect of his employment;

- any sum paid as statutory bonus or otherwise;

- any gratuity payable on discharge;

- any sum paid as reward or award, and any facility granted, or any sum in lieu thereof paid on a special occasion or performance;

- any payment for overtime;

- any sum paid to the employee to defray special expenses entailed by the nature of his employment;

- “year” means a total of three hundred and sixty-five days for which contributions are paid.

CHAPTER II INSURED PERSONS.

- Compulsory Insurance. —

(1) All employees in an industry or establishment shall compulsorily be insured in the manner prescribed by or under this Act.

(2) The self-employed persons, homemakers and overseas Pakistani workers may voluntarily get themselves insured under this Act in the prescribed manner.

(3) The minimum age for first-time registration for insurance under the Act shall be sixteen years, and the maximum age shall be fifty-eight years.

- Administration. —

(1) As soon as may be, after the commencement of this Act, the Government shall establish or nominate by notification an Institution to be called the Employees’ Old-Age Benefits Institution.

(2) The Institution shall be a body corporate having perpetual succession and a common seal, with powers, subject to the provisions of this Act, to acquire, hold and dispose of property, both movable and immovable, and shall by the aforesaid name sue or be sued.

- Nomination of a Body Corporate Pending Establishment of an Institution. —

(1) Notwithstanding anything contained in section 4, the Government may, pending the establishment of an Institution, by notification in the official Gazette, nominate a body corporate to exercise and perform all the powers and functions of the Institution under this Act and appoint the head of such body corporate, by whatever name called, to be the Chairperson of the Institution.

(2) The nomination of a body corporate under sub-section (1) shall be subject to such terms and conditions as the Government may, from time to time, determine.

- Management. —

(1) The general direction and superintendence of the affairs of the Institution shall vest in the Board, which may, with the assistance of the Chairperson of the Institution, exercise all powers and do all acts and things which may be exercised or done by the Institution.

(2) In discharging its functions, the Institution shall be guided by such instructions on questions of policy as may be given to it from time to time by the Government, which shall be the sole judge as to whether any instructions are on a question of policy or not.

- Board of Trustees. —

(1) The Board of Trustees shall consist of the following members to be appointed by the Government, by notification, namely: –

(a) the Secretary or Additional Secretary in the administrative Ministry, who shall also be the President of the Board of Trustees;

(b) four persons to represent the Federal Government, one each from the Ministries of Finance, Commerce, Industry and the administrative Ministry, not below the rank of Joint Secretary;

(c) four persons to represent the Provincial Governments, one to be nominated by each of the Provincial Governments, not below the rank of Secretary;

(d) four persons to represent employers;

(e) four persons to represent insured persons;

(f) two independent actuaries nominated by the Society of Actuaries; and

(g) two persons to represent the Institution.

(2) Members to be appointed under clause (d) and (e) of sub-section (1) shall respectively be chosen from a list of names submitted in the prescribed manner by the respective organisations of the employers and employees recognised by the Federal Government for that purpose.

- Powers and Functions of the Board of Trustees. —

In addition to the powers conferred on, and the functions entrusted to it by the other provisions of this Act or by the rules or by special instructions through notification by the Government, the Board shall have the following powers:

- to approve the budget estimates, the audited accounts and the annual report of the Institution for submission to the Government in accordance with the provisions of this Act;

- to review and, on or before the 30th day of May each year, recommend to the Government for approval the contribution base on which contributions shall be calculated under sections 10 and 12 of this Act for the next financial year and the minimum pension rate;

(b) to call for any information or direct any research to be made for the furtherance of the objects of the Act; and

(c) to co-opt any other technical person by name as a member on the Board for a specific purpose and for such limited period as decided by the Board:

Provided that such a member shall have no right to vote.

- Appointment, Powers and Functions of Chairperson. —

(1) The Chairperson of the Institution shall be appointed by the Government for such term and on such terms and conditions as it may determine.

(2) The Chairperson of the Institution shall exercise such powers and perform such functions as may be prescribed by the Rules.

CHAPTER III CONTRIBUTIONS

- Rates and Assessment. —

(1) The contributions shall be payable every month by the employer in respect of every person in his or her insurable employment at the rate of five per cent of the prescribed contribution base in the prescribed manner:

Provided that no contribution shall be payable in respect of or by an insured person who is in receipt of Old-age pension or Invalidity Pension under this Act or has attained the pensionable age.

(2) A self-employed person, an overseas Pakistani worker or other persons specified in section 1(4)(b) who voluntarily join the scheme shall pay a monthly contribution at the rate of six per cent of the prescribed contribution base, in such manner as may be prescribed.

(3) Where the wages are paid for part of the month, fortnight, week or a day, contributions shall be payable for the actual number of working days for which the wages are paid.

(4) Where an insured person does not receive any wages from the employer for any period, the Institution shall, subject to regulations, determine the amount of wages with reference to which the contributions shall be computed.

(5) Notwithstanding any agreement to the contrary, the employer shall not deduct from the wages of an insured person or otherwise recover from him or her any portion of the employer’s share of contribution.

(6) In the case of construction work, the owner of the building shall be responsible for ensuring that the contractor pays the contributions payable under this Act. Where the contractor fails to pay any such contribution, the owner shall be liable to pay the amount so determined by the Institution, in the prescribed manner.

(7) In the case of mine workers, the Board may consider special provisions for the computation of contributions on the basis of excavation and production of minerals, especially Coal.

(8) Where works are executed, or an undertaking is carried-on on behalf of the State by a contractor or licensee, the competent public authority shall, prior to settlement of each claim under the contract, require the contractor or licensee to produce a certificate issued by the Institution certifying that all contributions payable have been paid. In the absence of such a certificate, the competent public authority shall deduct from the amount otherwise payable in settlement of the claim the amount of the contributions payable, as determined by the Institution, and shall remit that amount directly to the Institution.

- Contribution by Government. — The Federal Government shall make a contribution to the Institution equal to the contributions paid by the employers and the insured persons after every quarter:

Provided that the amount paid as an increase by the employers due to late payment of contributions shall not be part of the payment under this section.

- Contribution by the insured person. —

(1) Contribution shall be payable by an insured person, other than those described in section 1(4)(b), at a fixed rate of one per cent of the contribution base determined under section 8 in the prescribed manner:

(2) If an insured person leaves the insurable employment for any reason whatsoever, except attaining the pensionable age, such an insured person may continue to pay his or her share of contribution along with the amount of employer’s share of contribution to be calculated under section 10, in the prescribed manner, and he or she shall be treated in insurable employment for the purpose of this Act.

(3) The self-employed persons and overseas Pakistani workers shall pay the contribution, as provided in section 10(2).

- Records and Returns by Employers. — Every employer shall keep such records and submit to the Institution such returns, at such times, in such form, and containing such particulars relating to persons employed by them, as may be provided in the regulations:

Provided that the employer shall keep such record for inspection by authorised officers of the Institution for a period not exceeding three years, or as advised in writing by the Institution in special circumstances.

- Registration of Establishment, etc. —

(1) Every employer shall, before the expiration of thirty days from the day on which this Act becomes applicable to the industry or establishment in respect of which he or she is the employer, communicate to the Institution the name and other prescribed particulars of the industry or establishment and of every insured person employed in the industry or establishment.

(2) Every insured person may also communicate his or her name and other prescribed particulars to the Institution, if his or her name is not communicated as provided in sub-section (1) above.

(3) On receipt of a communication under sub-section (1), the Institution shall register the name of the industry or establishment in such manner and issue a registration certificate in such form as may be prescribed.

(4) On receipt of a communication under sub-section (1) or sub-section (2), the Institution shall register the name of the insured person in such manner, and issue to the insured person a registration card in such form as may be prescribed.

(5). The self-employed persons, homemakers and overseas Pakistani workers who want to join the scheme voluntarily shall also provide such information as may be required under the regulations.

(4) On receipt of a communication under sub-section (5), the Institution shall register the name of the self-employed person or the overseas Pakistani worker in such manner, and issue a registration card in such form as may be prescribed.

(5) In case of failure of employers to perform their duties under sub-section (1), the authorised officer of the Institution may inspect the establishment or industry as provided under section 16, and the Institution may assess the contributions accordingly.

- Cancellation of Registration of Establishments, etc. — The Chairperson, on the basis of such evidence, according to the regulations and subject to clearance of all previous liabilities, may cancel the registration of any establishment or industry which has ceased to exist:

Provided that the cancellation of the registration of an establishment or industry shall not affect its liabilities incurred before the date of such cancellation:

Provided further that the cancellation of the registration of an establishment or industry shall take effect from the day of payment of all determined dues under the Act.

- Officials of the Institution to Check the Employer’s Books.-

(1) Any authorised official may, for the purpose of inquiring into the correctness of any of the particulars stated in the records or returns referred to in section 13 or for the purpose of ascertaining whether any of the provisions of this Act have been complied with: –

(a) at any reasonable time, enter any establishment or other premises occupied by such employer and require any person found in-charge thereof to produce and allow him or her to examine such books, registers and other documents relating to the employment of persons and payment of wages, or to furnish such information, as he or she may consider necessary; or

(b) require an employer to furnish such information as he or she may consider necessary; and

(c) examine, with respect to any matter relevant to the purposes aforesaid, the employer, his agent or any other person found in such establishment or other premises, or any other person whom the said official has reasonable cause to believe to be or to have been an insured person.

(2) The authorised official referred to in sub-section (1) shall be bound to secrecy as regards all matters with which he or she becomes acquainted in the performance of duties, and which do not relate to matters provided for in this Act.

(3) The official referred to in sub-section (1) shall not demand production of books and other documents referred to in clause (b) of sub-section (1) for a period beyond two years from the date of registration of the establishment or from the date of notice, whichever is later.

(4) If an employer fails to maintain records or to submit returns as required by the regulations, or otherwise fails to comply with the provisions of sub-section (1) and thereby makes it difficult to ascertain the identity of persons required to be insured or the amount of contribution payable, the contribution shall be assessed on the basis of such evidence as the Institution may find satisfactory for this purpose, in the prescribed manner:

Provided that prosecution shall be initiated against the employer for contravention of sub section (1) under section 47 of the Act.

(5) The number of annual inspections in respect of an establishment shall be restricted to only one, which shall be notified to such establishment in advance and shall be restricted to the last two years. Non-inspection of the books and records by the authorised official, for any reason, shall not justify a demand for the production of such books and records beyond the preceding two years.

- Increase of Unpaid Contribution and Recovery of Contribution, Etc., as arrears of land revenue. —

(1) If an employer fails to pay, on the due date, the contribution payable under sub-section (1) of section 10, the amount so payable shall be increased by such percentage or amount as may be prescribed:

Provided that in no case shall such increase exceed fifty per cent of the amount due:

Provided further that no increase shall be payable on late payment due under section 12 and no part of such increase shall be payable by, or the liability to pay the same shall be passed on by the employer to his or her employees:

Provided also that such increase shall not be payable by the employer who pays his unpaid contribution within one and a half years of the commencement of this Act (till 30 June 2027).

(2) Without prejudice to any other remedy, the amount of contribution due and the increase provided for under sub-section (1), may be recovered as arrears of land revenue.

- Safeguard of Insured Person’s Right in Default of Payment of Contributions by Employers: —

Notwithstanding anything contained in this Act, if an employed insured person has communicated his or her name and other prescribed particulars to the Institution under sub-section (2) of section 14 and, in case of changing employment from one industry or establishment to another industry or establishment, has also informed the Institution about such change of employment and paid his or her share of contribution under section 12 of the Act, then, in the event of default in payment of contributions by the employer in respect of such insured person, such insured person shall, unless he or she has connived at such default, have and enjoy the same rights under this Act as if no such default had occurred.

- Refund of Contributions Paid Erroneously. — An employer shall be entitled to the refund of any contribution paid to the Institution under erroneous belief that it was payable under the provisions of the Act, and shall be entitled to the refund of an excess amount of the contribution where such contribution had been paid at a higher rate than the rate prescribed or in respect of the persons not in insurable employment:

Provided that no contribution or excess amount of any contribution shall be refunded unless an application for such refund is made within two years of the date on which the contribution was paid or an order of the Court, whichever is later.

- Extinguishment of Claims to Contributions. — Any claims of the Institution for unpaid contributions shall be extinguished in the manner provided in the regulations.

CHAPTER IV FINANCE AND AUDIT

- Employees’ Old-Age Benefits Fund: —

(1) The Institution shall have its own fund, to be called the Employees’ Old-Age Benefits Fund, and may incur out of the Fund such expenditure as may be necessary for the purposes of this Act.

(2) All contributions paid under this Act and all other moneys received by or on behalf of the Institution shall be paid into the Fund.

(3) The Institution shall derive its revenues from the following sources:

(a) contribution payable under this Act and the rules;

(b) all other payments made by the employers, insured persons and the Government under this Act, rules and the regulations;

(c) income from investment of the moneys of the Institution; and

(d) donations, bequests and other miscellaneous payments for the purposes of this Act.

(4) The assets of the Institution shall be utilised solely for the purposes of this Act and for no other purpose whatsoever.

(5) The moneys of the Institution shall be deposited in such banks as may be approved by the Board for the purpose.

(6) The Institution shall maintain separate accounts for administrative expenses, and for benefits and such other purposes as may be prescribed.

- Investments and Loans. —

(1) Subject to rules, the Institution may, from time to time, invest any moneys which are not immediately required for expenses under this Act, and may re-invest or realize such investment.

(2) The Institution may, with the previous sanction of the Federal Government and on such terms as it may specify, raise loans and take measures for discharging such loans.

- Budget, Accounts and Audit. —

(1) The Institution shall, before such date and in such manner as may be prescribed, draw up estimates for the following year and shall submit them to the Board for the approval of the Government, containing the following details:

(a) the anticipated receipts of contributions and income from investments, etc.;

(b) the administrative expenses of the Institution;

(c) the expenditure to be incurred under each of the benefits and other purposes for which separate accounts are prescribed in accordance with sub-section (6) of section 21;

(2) The Institution shall maintain accounts of its income, expenditure, its assets and liabilities in such form and manner as may be prescribed.

(3) The books of account of the Institution shall be balanced on the thirtieth of June each year, and its accounts shall be audited by auditors approved by the administrative ministry on recommendation of the Board, at such time and in such manner as may be prescribed.

(4) The auditors shall at all reasonable times have access to the books of accounts and other documents of the Institution and may, for the purposes of the audit, call for such explanation and information as they may require and may examine any principal or other officer of the Institution.

(5) The auditors shall forward to the administrative ministry a report of their work and activities together with a copy of the accounts of the Institution for submission to the Government.

- Annual Report. — The Institution shall, within six months after the closing of each financial year, submit to the administrative ministry an annual report of its work and activities during that financial year, and such report shall cover matters as may be prescribed.

- Valuation of Assets and Liabilities. — The Institution shall, at intervals of not more than three years, have an actuarial valuation made in the prescribed manner of its assets and liabilities, and no change in the contribution base or benefit under this Act shall be made without proper actuarial valuation:

Provided that the administrative ministry may direct a valuation to be made at such other times as it may consider necessary:

Provided further that the actuarial valuation report shall be submitted to the Government within 30 days of its completion.

- Reports of the Institution. — The annual report, together with the audited accounts of the Institution and the actuarial report, shall be published, and printed copies thereof shall be made available for sale to the public. The published report shall also be made available online for free.

CHAPTER V BENEFITS

- Pensionable age. –

(1) Subject to Schedule II (Transitional Equalisation), pensionable age shall be sixty years:

Provided that the pensionable age shall be reduced by five years in the case of an insured person employed in a mine as defined in section 3(d), read with section 3(f) of the Mines Act, 1923, for at least ten years preceding attaining the pensionable age.

(2) Schedule II shall apply to any woman insured person who, immediately before the commencement of this Act, was so registered and would, but for the commencement of this Act, have become entitled to an old-age pension on attaining the age of fifty-five years.

(3) For the avoidance of doubt, pensionable age shall apply equally to all persons and shall not differ on the basis of sex, save only for transitional arrangements provided in Schedule II.

- Old-Age Pension. —

(1) An insured person shall be entitled to a monthly old-age pension at the rate specified in the schedule:

Provided that: –

(a) the insured person has attained the pensionable age; and

(b) contributions in respect of such insured person are paid for not less than fifteen years. A period of six months or more on insurable employment shall be treated as one full year.

Provided that where the contribution under section 12 is paid regularly by the insured person in accordance with the prescribed procedure, his or her entitlement to the benefit shall not be affected by default in payment of the employer’s share of contribution under section 10.

(2) An insured person already in receipt of an old-age or invalidity pension, or entitled to an old-age pension under the provisions of sub-section (1), shall be entitled to a minimum pension at the rate specified in Schedule I, if the pension calculates to be less than the minimum pension.

(3) An insured person who retired from insurable employment five years or less prior to attaining the pensionable age, shall be entitled to a reduced old-age pension on fulfilling the following conditions, namely:-

(a) the Institution is satisfied through documentary evidence that the employer has a definite established retirement age lower than the pensionable age set under section 27 and Schedule II;

(b) the employer certifies that the insured person has actually retired on attaining the age of superannuation, as per the employer policy; and

(c) the contributions in respect of such insured person are paid for the period required under the provisions of this Act.

(4) The old-age pension under sub section (3) shall be reduced by one-half per cent of the Old-Age Pension specified in the Schedule for each completed month by which the age falls short of pensionable age and the minimum old-age pension shall also be reduced in the aforesaid manner.

(5) The reduction in old-age pension specified in sub-section (4) shall be for life and shall not be restored on the insured person’s attaining the normal pension age.

(6) Subject to regulations, the old-age pension shall commence as from the month following that in which the insured person satisfies the condition for entitlement thereto, provided that no Benefit shall be payable retroactively for more than twelve months preceding the month in which an application for old-age pension is submitted.

(7) Insurable employment of a person for the purposes of this Act shall commence on the date from which the first contribution by or in respect of the insured person was paid.

(8) The old-age pension payable to an insured person shall be terminated at the end of the month in which the death of such a person occurs.

(9) The self-employed persons, homemakers and overseas Pakistani workers who pay the contribution shall be entitled to Old-age Pension, in the above manner.

(10) Any insured person may opt for enhanced Old-age Pension on payment of enhanced contributions, including the employer’s contribution under section 10, as may be prescribed by rules.

- Old-Age Grant. —

(1) If an insured person, not otherwise entitled to old-age pension, attains the pensionable age, and contributions in respect of such insured person were paid for less than fifteen years, but not less than two years, such an insured person shall be entitled to an old-age grant payable in a lump sum equal to last contribution base for every completed year of insurable employment or part thereof in excess of six months:

Provided a period of six months or more on insurable employment shall be treated as one full year:

Provided further that in case of the death of an insured person who had become entitled to Old-age Grant or has received the Old-age Grant on the basis of more than five years of insurable employment, the survivors shall be entitled to Survivors’ Pension, subject to fulfilment of other requirements as per section 30.

(2) The self-employed persons, homemakers and overseas Pakistani workers who meet the above conditions shall be entitled to the Old-age Grant.

- Survivors’ Pension. —

(1) In the case of the death of an insured person while in insurable employment, in respect of whom contributions are paid for at least thirty-six months, the surviving spouse, if any, shall be entitled to a life pension equal to the minimum pension:

Provided that for the purpose of entitlement to Survivors’ Pension under this section, a period of fifteen days or more of insurable employment shall be treated as one month.

(2) In case of the death of an insured person, while not in insurable employment but after he or she had completed five years of insurable employment before his or her death, the surviving spouse, if any, shall be entitled to a life pension equal to the minimum pension, irrespective of the fact that the deceased has received the old-age grant. A period of six months or more of insurable employment shall be treated as one full year.

(3) In the case of the death of an insured person who had become entitled to old-age pension, invalidity pension or in receipt of such pension before death, the surviving spouse shall receive a life pension equal to the pension of such person.

(4) In case of the death of the surviving spouse who was in receipt of a survivor’s pension, the minor children of the deceased insured person, if any, shall be entitled to the survivor’s pension, in the following equal shares, namely:

(i) In case of a male child, until he attains eighteen years of age;

(ii) In case of a female child, a widowed or divorced daughter, until her marriage; and

(iii) In the case of a disabled person, for life.

(5) In the case of cessation of survivor’s pension of any of the children of the deceased insured person on attaining the age of eighteen years in case of a male or marriage in case of a female, or death, as the case may be, the share of survivor’s pension received by such child shall be distributed equally among the other recipients of the pension share.

(6) In case of death of the surviving spouse in receipt of a survivor’s pension within ten years after the death of the insured person and not survived by any minor or disabled child or unmarried daughter of the deceased insured person, the survivor’s pension shall be paid to the surviving parents of the deceased insured person, if any, for a period of ten years from the death of said spouse or death of such parent whichever is earlier:

Provided that, if both parents are alive, the pension shall initially be granted to the father, and upon his death, it shall be transferred to the mother for the remainder of the period.

(7) In case of the death of an insured person who is not survived by a spouse, the survivor’s pension shall be paid to the children of the deceased insured person referred to in sub-section (4) and in the case of the insured person not survived by any child or unmarried daughter, the survivor’s pension shall be paid to the surviving parent, if any, for a period of twenty years from the death of insured person or death of such parent whichever is earlier:

Provided that, if both parents are alive, the pension shall initially be granted to the father, and upon his death, it shall be transferred to the mother for the remainder of the period.

(8) Subject to regulations, the survivors’ pension shall commence as from the month following that in which the insured person dies, provided that no pension shall be payable retroactively for more than twelve months preceding the month in which an application for survivors’ pension is submitted.

(9) The survivors of self-employed persons, homemakers and overseas Pakistani workers shall also be entitled to the Survivors’ Pension accordingly.

- Invalidity Pension. —

(1) An insured person who sustains invalidity shall be entitled to an invalidity pension at the rate to be calculated according to the formula set out in the schedule:

Provided that:-

(a) contributions in respect of such insured person are paid for not less than fifteen years; or

(b) contributions in respect of such insured person are paid for not less than five years since his or her entry into insurable employment and for not less than three years during the period of five years preceding the month in which he sustains invalidity; and

(c) in either case, the insured person has not attained the pensionable age.

Provided further that where the contribution under section 12 is paid regularly by the insured person himself or herself in accordance with the prescribed procedure, the entitlement to the benefit shall not be affected by default in payment of the employer’s share of contribution under section 10.

(2) Subject to regulations, the invalidity pension shall be payable from the month following that in which the insured person satisfies the conditions for entitlement thereto:

Provided that the invalidity pension shall not be payable retroactively for more than twelve months preceding the month in which an application for the invalidity pension is submitted.

(3) The invalidity pension shall be payable so long as invalidity continues:

Provided that an insured person who has been in receipt of the invalidity pension for not less than five continuous years or attains the age specified in sub-section (3) of section 28 shall be entitled to the invalidity pension for life.

(4) The self-employed persons, homemakers and overseas Pakistani workers shall also be entitled to Invalidity Pension accordingly.

CHAPTER VI PROVISIONS COMMON TO ALL BENEFITS

- 32.Calculation of Qualifying Contribution Periods. — n calculating the contribution periods for entitlement to any benefit under this Act, periods in respect of which invalidity pension has been paid to an insured person prior to his reaching the pensionable age, or periods in respect of which maternity benefit or sickness benefit or injury benefit or total disablement pension have been paid under the West Pakistan Employees’ Social Security Ordinance, 1965 (West Pakistan Ordinance No. X of 1965), or its provincial variants, to an insured person shall be deemed to be contribution periods under this Act.

- Care Credits for Caregiving Periods

(1) Notwithstanding anything contained in this Act, the Institution shall credit care credits to an insured person’s contribution record in accordance with this section and the rules.

(2) Care credits shall be available to an insured person who satisfies the prescribed conditions.

(3) For the purpose of subsections (1) & (2), the following periods shall be credited in the entire insurable employment:

(a) 3 months of care credit for each child born alive, with a maximum of 6 months for all children, when the number of children exceeds two; and

(b) an additional one month of care credit for each child with disability, subject to certification in the prescribed manner;

(4) The Institution may credit the care credits to an insured person’s contribution record for periods of intensive care provided to a person with severe disability or to an elderly person requiring intensive care, with a maximum period of 3 months in the entire period of insurable employment, as may be prescribed.

(5) The total childcare credits and Intensive care credits that may be credited under this section shall not exceed 12 months.

(6) Care credits credited under this section shall:

(a) count as insurable employment for purposes of meeting minimum qualifying service; and

(b) be treated as a contribution period for purposes of benefit calculation,

in the manner prescribed; and no employer contribution liability shall arise in respect of such care credits.

(7) For child-rearing credits, the parents/guardians may nominate a designated caregiver in the prescribed manner; in default, the mother shall be deemed the designated caregiver unless the contrary is established under the rules.

(8) Care credits shall be credited on the basis of civil records and other evidence as may be prescribed, including records maintained by NADRA and such other notified authorities.

(9) Any person who knowingly makes a false statement or furnishes false evidence to obtain care credits commits an offence punishable with a fine of ten thousand rupees, and any care credits wrongly credited shall be recoverable as arrears of land revenue.

- Benefits claims and payments. —

(1) All claims for a benefit under this Act shall be made in writing and shall be accompanied by such documents, information and evidence as to entitlement as may be provided by regulations.

(2) Payment of a benefit shall be made in such manner, and at such times and places, as may be provided by regulations.

- Extinguishment of Benefits. — A right to any benefit shall stand extinguished where a claim therefore is not made within three years of the date on which the benefit becomes payable:

Provided that the Institution may condone the delay and admit the claim if it is satisfied that the delay was caused for reasons beyond the control of the insured person or the survivor.

- Payment of Benefits outside Pakistan. — All benefits, provided under Chapter IV, shall be paid to beneficiaries inside and outside Pakistan, in Pakistani currency, through official banking channels. Payment of benefits shall not be suspended by reason only of the beneficiary’s absence from Pakistan or residence abroad. The Institution shall prescribe secure digital or consular life-certification procedures.

- Non-Duplication of Benefit. —

(1) An insured person shall not be paid for the same period more than one of the benefits provided under this Act.

Provided that, for the purpose of duplication, the survivors’ benefit to an insured person shall not be treated as a duplicate benefit under the Act.

(2) Where an insured person is entitled to more than one benefit under this Act, such person shall be given the higher of such benefits.

- Benefit Not Attachable, Chargeable or Assignable. — A benefit payable under this Act shall not be liable to attachment in the execution of a decree, nor shall it be chargeable or assignable; and any agreement to charge or assign a benefit shall be void, and on the bankruptcy of an insured person, the benefit payable to him or her shall not pass to any trustee or person acting on behalf of such person’s creditors.

- Repayment of benefit Improperly Received. —

(1) When a person has received any benefit under this Act to which such person is not lawfully entitled, he or she shall be liable to repay to the Institution the amount of the benefit in such manner as may be provided by regulations:

Provided that the Institution may waive repayment of a benefit where payment thereof was not due to misrepresentation on the part of the person receiving it, and the repayment would cause undue hardship to him or her.

(2) Sums due to the Institution by virtue of the foregoing sub-section may be recovered by deduction from a benefit payable under this Act or as arrears of land revenue.

- Institution’s Right to Be Indemnified in Certain Cases. —

(1) Where the contingency for which a benefit is payable under this Act was caused under circumstances creating a legal liability in some person, the Institution shall be entitled to substitute itself for the insured person in bringing a suit for recovery or damages against that person.

(2) Where any employer has failed to pay contributions in respect of any insured person, and due to failure on the part of the employer, such insured person, who is otherwise entitled to any benefit under this Act, is being deprived of, the Institution may assess and recover the due amount from such employer.

- Recovery of Amounts Due. — Any amount recoverable under this chapter may be recovered as arrears of land revenue.

CHAPTER VII DETERMINATION OF QUESTIONS AND CLAIMS

- Decision on Complaints, Questions and Disputes. —

If any complaint is received or any question or dispute arises as to-

(a) whether a person is an insured person within the meaning of this Act;

(b) the amount of due contribution payable by an employer in respect of insured persons;

(c) the person who is or was the employer in respect of an insured person;

(d) entitlement to any benefit under this Act or as to the amount and duration thereof;

(e) registration of industry or establishment; and

(f) any other matter in respect of any contribution or any benefit under the Act, or other dues payable or recoverable under this Act relating to contributions or the benefits;

the matter shall be decided by the Institution, in such manner, and within such time, as the regulations may provide, and the Institution shall notify its decision to the person concerned in writing, stating therein the reason for its decision.

- Review on account of new facts. — The Institution may, subject to regulations, on its own motion or on new facts being brought to its notice, review a decision given by it under section 42:

Provided that no decision shall be so reviewed without giving the person concerned an opportunity of being heard and adducing evidence in support of, or against, the decision, as the case may be.

- Appeal.– Any person aggrieved by a decision of the Institution under section 42 or on a review under section 43 may appeal to the appropriate Pension Court.

- Constitution of Pension Court.– (1) The Government may, for purposes of this Act, constitute a Pension Court or designate any Labour or Civil Court to be a Pension Court for any Area or Areas specified in the notification.

(2) A Pension Court shall be presided over by a Judge who shall be appointed by the Government.

(3) A person shall not be appointed as a Judge of a Pension Court unless such person has–

(a) for a period of not less than three years held a judicial office; or

(b) for a period, or for periods aggregating not less than seven years, have been an advocate or pleader of the High Court.

- Jurisdiction of Pension Courts.– (1) Subject to the provisions of subsection (2), a Pension Court shall have exclusive jurisdiction to hear and decide appeals from decisions of the Institution under section 42 or reviews under section 43 in respect of all claims, questions and disputes arising in the appropriate Area of its jurisdiction.

(2) The Government may, by order in writing, transfer an appeal from one Pension Court to another, whenever it appears to it that such transfer will promote the ends of justice or tend to the general convenience of the parties and witnesses.

(3) The Pension Court to which an appeal has been transferred under the provisions of sub-section (2) shall deal with the same as if it had been originally instituted in, or presented to, such Court.

- Powers of Pension Court, etc.– (1) A Pension Court shall have all the powers of a Civil Court for the purposes of summoning and enforcing the attendance of witnesses, compelling the discovery and production of documents and material objects, administering oath and recording evidence, and such a Court shall be deemed to be a Civil Court within the meaning of section 195 of the Code of Criminal Procedure, 1898 (Act V of 1898).

(2) Notwithstanding anything contained in any other law, a Pension Court may, for the purpose of deciding any appeal, examine such witnesses and take such evidence as it considers necessary.

(3) A Pension Court may make such an order with regard to costs incidental to any appeal as it thinks fit.

(4) An order of a Pension Court shall be enforceable as if it were a decree of a Civil Court.

(5) A person shall be guilty of contempt of a Pension Court if such a person, without lawful excuse–

(a)offers any insult to the Pension Court or any member thereof while the Court is functioning as such;

(b) or causes any interruption in the work of the Pension Court; or

(c) fails to produce or deliver a document when ordered by the Pension Court to do so; or

(d) refuses to answer any question of the Pension Court which he is bound to answer; or

(e) refuses to take oath to state the truth or to sign any statement made by him when required by the Pension Court to do so;

and the Pension Court may, without any complaint having been made to it, forthwith try such person for such contempt and sentence him to a fine not exceeding fifty thousand rupees.

- Appearance by legal practitioners.– Any application, appearance or act required to be made or done by any person to or before a Pension Court (other than the appearance of a person required for the purposes of examination as a witness) may be made or performed by such person, or by a legal practitioner or by an officer of a registered trade union authorised in writing by such person, or, with the permission of the Court by any other person so authorised.

- Finality of Order.– (1) Save as expressly provided in this section; no appeal shall lie from an order of a Pension Court.

(2) An appeal shall lie to the High Court from an order of a Pension Court only if it involves a substantial question of law.

(3 The period of limitation for an appeal under this section shall be thirty days.

(4) The provisions of sections 5 and 12 of the Limitation Act, 1908 (IX of 1908) shall apply to appeals under this section.

- Stay of payment pending appeals.– Where any person has appealed against an order of a Pension Court, that Court may, and, if so directed by the High Court, shall, pending the decision of the appeal, direct that the payment of any sum required to be paid by the order appealed against shall be withheld.

- Assessment of Invalidity. — The Institution shall appoint medical boards which shall, in such manner as may be provided by regulations, assess the degree of invalidity sustained by an insured person.

CHAPTER VIII OFFENCES AND PENALTIES

- Offences. —

If any person

(a) for the purpose of obtaining a benefit or denial of any payment or benefit, under this Act, whether for themselves or some other person, or for the purpose of avoiding any payment to be made by themselves or any other person under this Act.

(i) knowingly makes or causes to be made a false statement or false representation; or

(ii) produces or furnishes, or cause, or knowingly allows to be produced or furnished, any document or information which he knows to be false in any material particular; or

(b) fails to pay any contribution which, under the Act, he or she is liable to pay; or

(c) recovers or attempts to recover from an insured person, or deducts or attempts to deduct from the insured person’s wages, the whole or any part of the employer’s share of contribution; or

(d) fails or refuses to submit any return required by this Act, or regulations or makes a false return; or

(e) obstructs any official of the Institution in the discharge of his or her duties; or

(f) is guilty of any contravention of, or non-compliance with, any of the provisions of this Act or the rules or the regulations,

such person shall be punished with imprisonment for a term which may extend to six months, or with a fine which may extend to ten thousand rupees in each count, or with both.

- Prosecution. —

(1) No prosecution under this Act shall be instituted except with the previous sanction of the administrative ministry or any officer or authority authorized in this behalf by it.

(2) No court other than the Pension Court shall try any offence under this Act.

(3) The Pension Court shall take cognizance of any offence under this Act on a complaint made in writing within twelve months of the date on which the offence comes to the knowledge of the Institution, administrative ministry or any officer or authority referred to in sub-section (1).

(4) All cases under this section shall be tried summarily.

CHAPTER IX

MISCELLANEOUS

- Contributions Etc. — In any proceedings of insolvency against a person or proceedings for winding up of a company, any contribution or other amount payable under this Act by such person or company shall be deemed to be included among debts to be paid in priority to all other debts.

- Exemption From Stamp Duty. — Stamp duty shall not be chargeable upon any document used in connection with benefits payable under this Act.

- Exemption From Federal Taxes. — Notwithstanding anything contained in any other law, the Federal Government may, by order in writing, exempt the Institution from any tax, duty, or rate leviable by the Federal Government or by a local authority under the control of the Federal Government.

- Exemption From Provincial and Local Taxes. — Notwithstanding anything contained in any other law, the Provincial Governments may, by order in writing, exempt the Institution from any tax, duty, or rate leviable by the Provincial Governments or by a local authority under the control of such Provincial Governments.

- Members and Servants of the Institution to Be Public Servants. — The members and employees of the Board and all officers and servants of the Institution shall be deemed to be public servants within the meaning of section 21 of the Pakistan Penal Code (Act XLV of 1860).

- Delegation of Powers. — The Board may direct that all or any of its powers and functions may, in relation to such matters and subject to such conditions, if any, as may be specified, be also exercisable by any officer or authority subordinate to the institution:

Provided that such authority cannot sub-delegate such delegated powers without prior written approval of the Board or any resolution in this behalf.

- Power to Make Rules. —

(1) The Government may, subject to the condition of previous publication in the official Gazette, make rules not inconsistent with the provisions of this Act, to carry out the purposes of this Act.

(2) In particular, and without prejudice to the generality of the foregoing power, such rules may provide for all or any of the following matters, namely: –

- the tenure of office of members of the Board, other than the President, the representatives of federal and provincial ministries and other terms and conditions of appointment of the members of the Board and the manner in which the Board shall conduct its business, including the number of members required to form a quorum at the meetings thereof;

- the manner in which names of persons from whom members of the Board may be appointed shall be submitted by organizations of employers and employees recognized by the Federal Government and the Society of Actuaries for the purpose;

- powers and functions of the Board.

- fees and allowances of the members of the Board;

- investment of surplus moneys, realisation of investments and reinvestment of proceeds;

- terms at which and the manner in which the budget of the Institution shall be prepared and submitted to the Government;

- the form and manner in which the Institution shall keep accounts of its income and expenditure and of its assets and liabilities;

- the times at which, and the manner in which, the accounts of the Institution shall be audited;

- the matters which the annual report of the Institution shall cover;

- the manner and procedure for disposal of appeals by the Board;

- the manner in which the services of the employees of the Institution shall be organised; and

- any other matter which is required to be or may be prescribed.

- Power to Make Regulations. —

(1) The Board may, subject to the condition of previous publication, by notification in the official Gazette, make regulations not inconsistent with the provisions of this Act or the rules.

(2) In particular, and without prejudice to the generality of the foregoing power, such regulations may provide for all or any of the following matters, namely: –

- the time and places at which meetings of the Board shall held;

- records to be kept and returns to be submitted by employers, the time at which and the form in which such returns are to be submitted, and particulars relating to the insured persons to be stated in such returns and the manner and form for registration of employers and insured persons;

- the manner in which any claim of the Institution for unpaid contributions may be extinguished;

- powers and duties of internal auditors.

- the form and manner in which claims for a benefit shall be preferred, and the documents, information and evidence which shall accompany such claims;

- the manner in which and the time and places at which payment in respect of a benefit shall be made;

- the manner in which and the time within which complaints, questions and disputes shall be decided;

- the circumstances and the manner in which, on new facts coming to light, the Institution may review decisions;

- the manner in which invalidity shall be assessed and the procedure thereof;

- the manner in which proof of age shall be furnished for the purposes of this Act;

- the manner in which the contribution base shall be reviewed and recommended every year by the Board for approval of the Government;

- the manner in which the amount of minimum pension shall be reviewed and recommended by the Board;

- the manner in which a yearly statement of contributions received in respect of the insured person shall be provided; and

- any other matter not provided for in this Act or the rules and necessary to give effect to the provisions of this Act.

- Provision of yearly statement of contribution. — The Institution shall provide a yearly statement of contributions received in respect of the insured person on payment of a fee or otherwise as prescribed by the Board.

- Issuance of instruction, circular, policy or SOP etc. — The Institution shall not issue any instruction, circular, policy or SOP in whatsoever nature on the matters enumerated in sections 53 and 54 except in the nature of a Rule or Regulation.

- Power to Exempt. — The Government may, subject to such conditions as it thinks fit to impose, by notification in the Official Gazette, exempt any person, establishment or industry from all or any of the provisions of this Act.

- Act Not to Apply to Certain Persons. — Nothing in this Act shall apply to:

(a) persons in the service of the state, including members of the armed forces, police force and railway servants

(b) persons in the service of the local council, a municipal committee, a cantonment board or any other local authority except self-employed persons;

(c) persons who are employed in services or installations connected with or incidental to the Armed Forces of Pakistan, including an ordinance factory maintained by the Government or the Railway Administration;

(d) persons in the service of the Water & Power Development Authority and other statutory bodies who have their own statutory pension rules;

(e) members of the employer’s family, that is to say, the husband or wife and the dependent children of the employer living in his house, in respect of their work for him.

- Repeal. —

(1) The Employees Old-Age Benefits Act 1976 (XIV of 1976) is hereby repealed.

(2) Notwithstanding such repeal:

(i) anything done, any rules, regulations or schemes made, or any order, notice or notification issued or any Chairperson, member or officer appointed, or any committee or fund constituted, or any notice given, any other action or proceedings taken or commenced shall, subject to conformity with the provisions of this Act, remain in force and shall be deemed to have been done, made, issued, appointed, constituted, given, filed, submitted, granted, taken or commenced under the corresponding provision of this Act, until repealed, or amended;

(ii) any case or proceedings pending in any Court or Tribunal or authority at the time of commencement of this Act shall be continued in and heard and disposed of by such Court or Tribunal, as if such laws were not repealed; and

(iii) any reference to the repealed Act shall be construed as a reference to the corresponding provisions of this Act.

SCHEDULE I

(See sections 27, 29 & 30)

- The monthly rate of old-age pension, invalidity pension or survivors’ pension payable to an insured person shall be calculated in accordance with the following formula, namely: –

(Last contribution base on which contribution is paid) x Number of years of insurable employment)

50

i.e. to say 2% of the last contribution base for each year of insurable employment.

- The contribution base for an insured person, referred to in paragraph (1), shall be that on which last contribution was paid immediately preceding the date on which the insured person fulfils the conditions for entitlement to any benefits under this Act.

- A period of six months or more of the insurable employment shall be treated as one full year:

Provided that the old-age pension, invalidity pension or survivors’ pension payable to an insured person or survivor of an insured person shall not be less than the minimum pension.

SCHEDULE II

(See sections 27 & 28)

TRANSITIONAL EQUALISATION OF PENSIONABLE AGE

- Interpretation.—In this Schedule, “commencement date” means the date on which the Employees’ Old-Age Benefits Act, 2026 comes into force.

- General rule.—This Schedule applies only to a woman insured person described in section 28(1)(a).

- Transitional pensionable age.—Notwithstanding section 28(1)(a), the pensionable age for a person to whom this Schedule applies shall be determined by reference to the date on which that person attains the age of fifty-five years, as follows:

(a) if the person attained the age of fifty-five years

before the commencement date, pensionable age is

fifty-five years;

(b) if the person attains the age of fifty-five years

on or after the commencement date but before the first anniversary of the commencement date, pensionable age is

fifty-five years and six months;

(c) if the person attains the age of fifty-five years

on or after the first anniversary but before the second anniversary of the commencement date, pensionable age is

fifty-six years;

(d) if the person attains the age of fifty-five years

on or after the second anniversary but before the third anniversary of the commencement date, pensionable age is

fifty-six years and six months;

(e) if the person attains the age of fifty-five years

on or after the third anniversary but before the fourth anniversary of the commencement date, pensionable age is

fifty-seven years;

(f) if the person attains the age of fifty-five years

on or after the fourth anniversary but before the fifth anniversary of the commencement date, pensionable age is

fifty-seven years and six months;

(g) if the person attains the age of fifty-five years

on or after the fifth anniversary but before the sixth anniversary of the commencement date, pensionable age is

fifty-eight years;

(h) if the person attains the age of fifty-five years

on or after the sixth anniversary but before the seventh anniversary of the commencement date, pensionable age is

fifty-eight years and six months;

(i) if the person attains the age of fifty-five years

on or after the seventh anniversary but before the eighth anniversary of the commencement date, pensionable age is

fifty-nine years;

(j) if the person attains the age of fifty-five years

on or after the eighth anniversary but before the ninth anniversary of the commencement date, pensionable age is

fifty-nine years and six months; and

(k) if the person attains the age of fifty-five years

on or after the ninth anniversary of the commencement date, pensionable age is

sixty years.

- No change to pensionable age or the transitional timetable shall have effect except by Act of Parliament.

- No detriment to accrued entitlement.—Nothing in this Schedule affects entitlement to an old-age pension that arose before the commencement date.

STATEMENT OF OBJECTS AND REASONS

The Constitution of Pakistan enshrines social protection as a fundamental right, primarily through

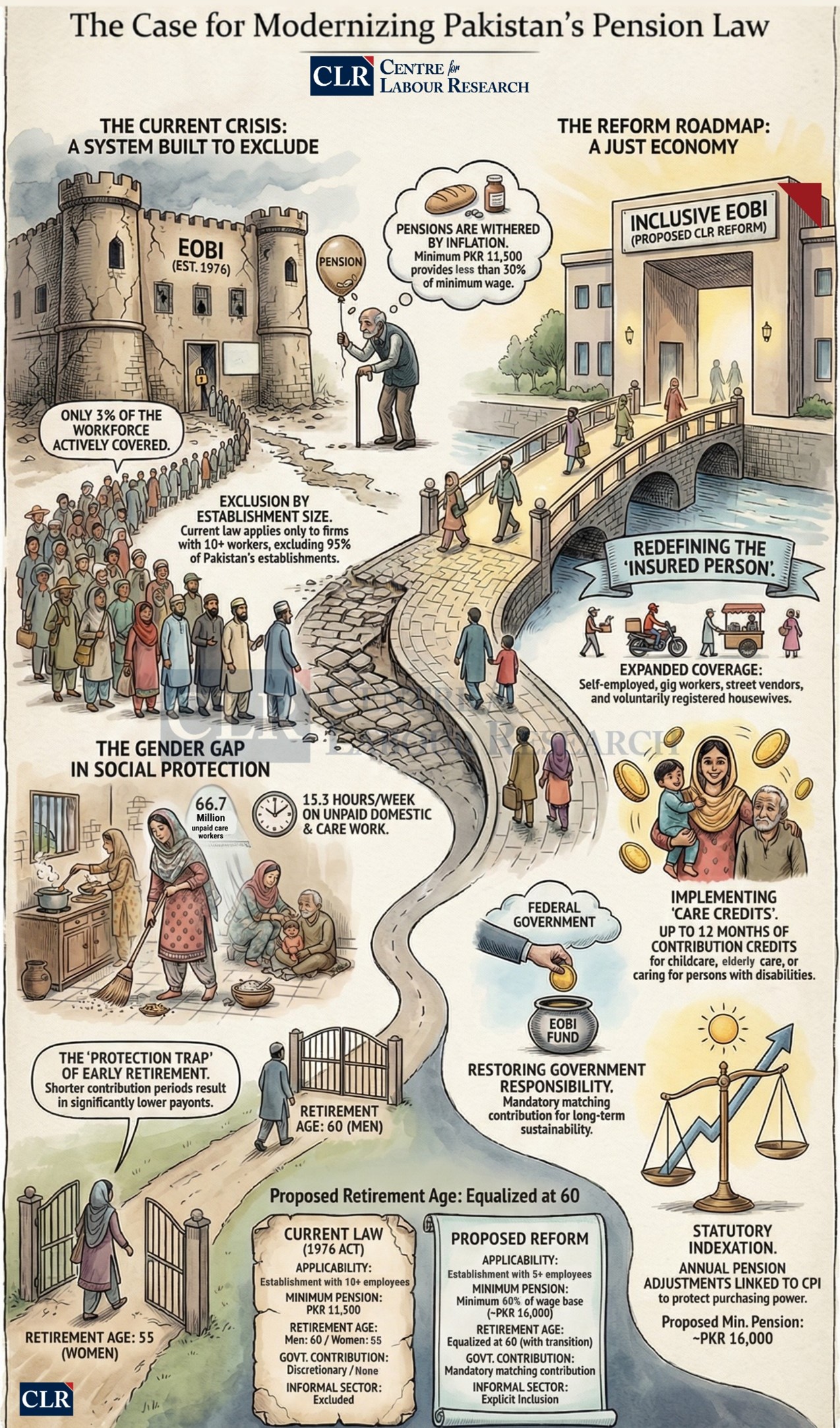

Article 38 in the Principles of Policy section, which mandates the State to secure the well-being of its citizens. Under this obligation, the “Employees’ Old-Age Benefits Act, 1976” was promulgated. After its enactment in 1976, many amendments were made to it. The first amendment was made in 1983 through the Employees’ Old-Age Benefits (Amendment) Ordinance, 1983. Thereafter, until June 2008, this law was amended by various statutes in 1983, 1985, 1986, 1993, 1994, 1995, 2000, 2001, 2002, 2005, 2006, 2007, and 2008. Amongst these, the amendments made in 1986, 1995, 2005, 2006, 2007, and 2008 were through Finance Acts. The Hon’able Supreme Court of Pakistan (in 2017) and all the provincial High Courts (in 2012) ruled that

all amendments made in the labour laws, including the EOB Act, at least in the years 2005, 2006, 2007 and 2008, are ultra vires to the Constitution of Pakistan. These decisions have made the existing Employees’ Old-age Benefits Act, 1976, practically unimplementable,

and they require firm steps to ensure the survival and sustainability of both the scheme and the Institution. The case law regarding the assessment and recovery of contributions, the limit of wages for the computation of contributions, the calculation of age for the payment of benefits, etc., is vital for a proper appreciation of the law and the practice being carried on by the Institution.

While High Courts in Sindh and Balochistan decided that the contribution was payable at 6% of the prevalent minimum wage, the High Courts in Lahore and Islamabad, as well as the Peshawar High Court, have decided that the contribution by the employer is payable at 5% of Rs 3,000, the wage limit set under section 9 before the 2005 amendment to the Act. The latter courts have relied on a proviso of the EOB Act, 1976 that states: “Provided that no contribution shall be payable on so much of an insured person’s wages as in excess of Rs 3,000”. Although this proviso was omitted through the Finance Act, 2005, it was later restored by the Supreme Court judgement of 2017. The current situation, where various employers are paying a contribution of Rs. 170 at Rs. 3,000 (Rs. 150 from the employer and Rs. 20 from the worker) instead of Rs. 2,400 (Rs. 2,000 from the employer and Rs. 400 from the worker) at the Rs. 40,000 (the current minimum wage for unskilled workers) is creating financial precarity for the institution and its current and future beneficiaries. To end this chaotic situation and the wrangling between employers and EOBI, reform is needed.

In view of the above, the Bill to repeal and re-enact the Employees’ Old-age Benefits Act, 1976, is being introduced to put the Scheme as well as the Institution back on track and to give legal cover to the computation of contribution, payment of benefits, and the minimum pension. The Bill introduces and provides legal protection to the self-registration scheme, includes special provisions for domestic workers, home-based workers, platform workers, part-time workers, overseas Pakistani workers, and homemakers, especially housewives, and introduces a package scheme for insured persons who want to receive higher benefits at the time of retirement.

The Bill also provides a special formula for calculating contributions for mine workers on a production basis and allows welfare associations to register themselves as employers in respect of their members and pay contributions on their behalf. This will bring a large number of informal sector workers into the scheme.

To enhance the revenue of the Institution, the Bill proposes to introduce a minimum age for registration as sixteen years and a maximum age of fifty-eight years. This will provide an opportunity for the registration of young workers, given that the minimum age for employment is sixteen years. Similarly, it provides for self-contribution in the event of a change of employment to a non-registerable establishment or of being unemployed, and eliminates various unnecessary exclusions set out in section 47 of the EOB Act 1976. These features will not only provide new avenues for contributions but also expand the coverage of eligible persons to have social protection under this law.

Member In-Charge

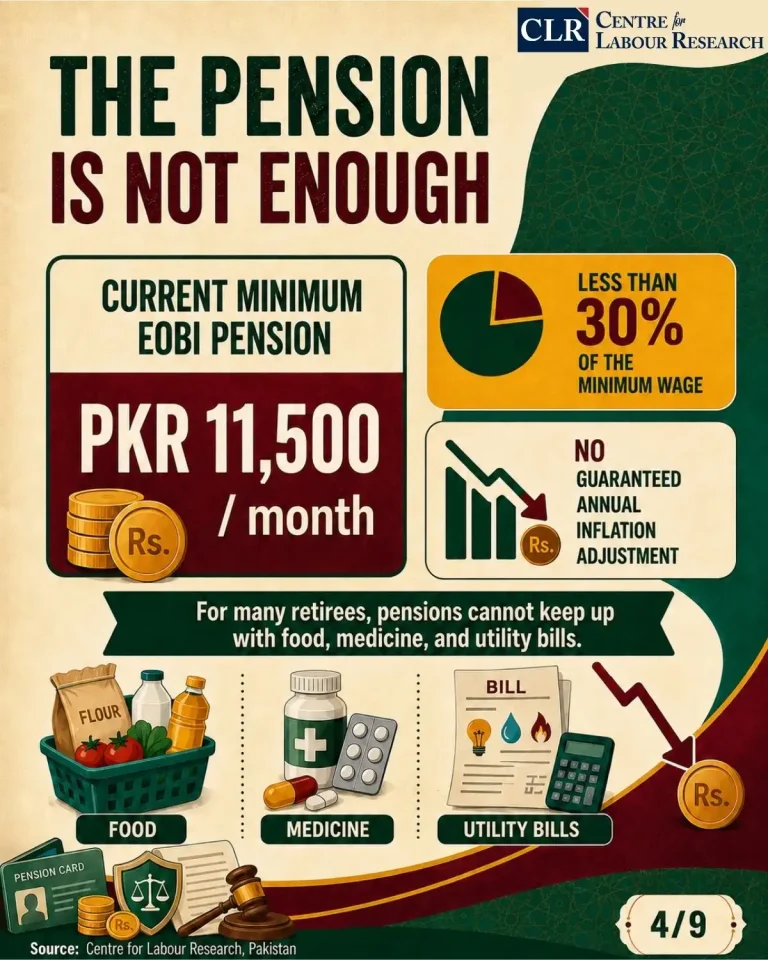

From the viewpoint of ILO Convention No. 102 and Recommendation No. 202, this is a serious flaw. Both instruments emphasize not only adequacy at the time of award, but also the regular adjustment of benefits to maintain purchasing power and a decent standard of living over time. A scheme that allows pensions to wither in real terms between irregular, politically expedient adjustments does not meet that test.

Before 2010, the federal government made several amendments to the EOBI Act 1976 through Finance Acts. However, in later years, the High Courts and the Supreme Court held that these amendments were ultra vires the Constitution, effectively restoring the legal position to its pre-2005 state. But that would mean the total contribution payable to EOBI would be only PKR 170 (PKR 150 from the employer + PKR 20 from the worker), instead of PKR 2400 per month. This would make EOBI severely underfunded and unsustainable.

Given this background, the Centre for Labour Research has been preparing a draft to amend and reenact the EOBI law to align it with international standards and the labour market’s needs.

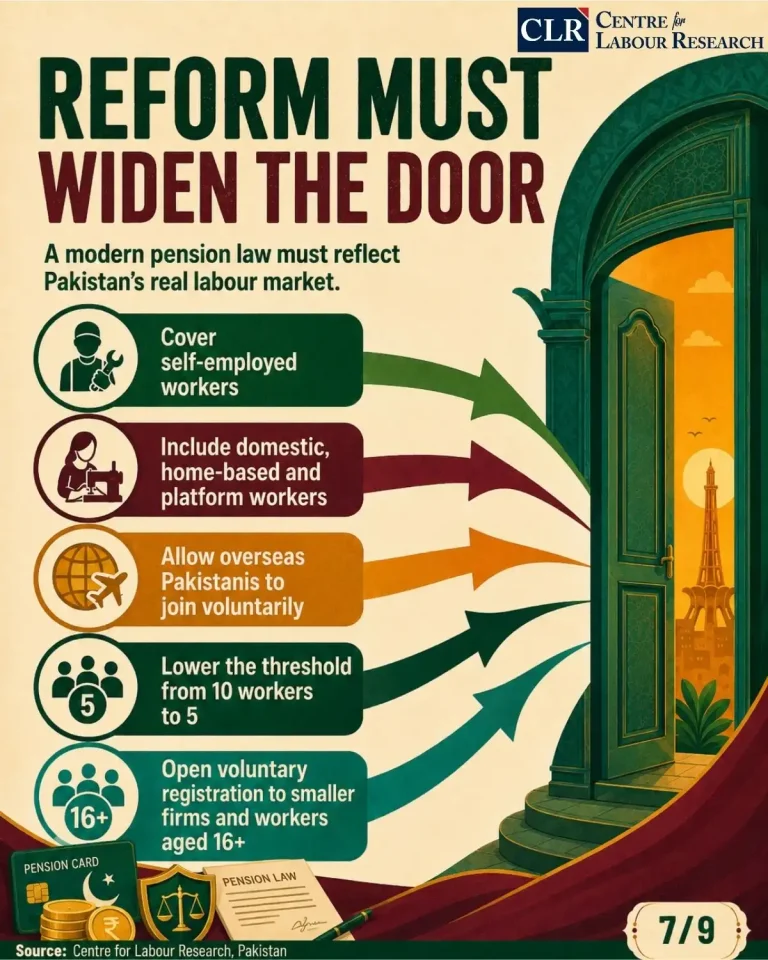

Scope of “insured person”: ILO Convention No. 102 mandates coverage of at least 50% of all employees or 20% of economically active residents. The Social Protection Floors Recommendation (No. 202) calls for universal coverage, ensuring that all residents have access to at least basic social security guarantees. Under current law, an insured person is essentially an employee in insurable employment (i.e., a contract of service/apprenticeship). Under the amendment proposal, the term “insured person” includes employees and the self-employed. The definition of “self-employed” explicitly includes platform workers, online freelancers, street vendors, domestic workers, home-based workers, and other informal sector workers. It also allows overseas Pakistani workers to be registered with the EOBI. Both the self-employed and overseas Pakistani workers can voluntarily register themselves with EOBI and self-contribute.

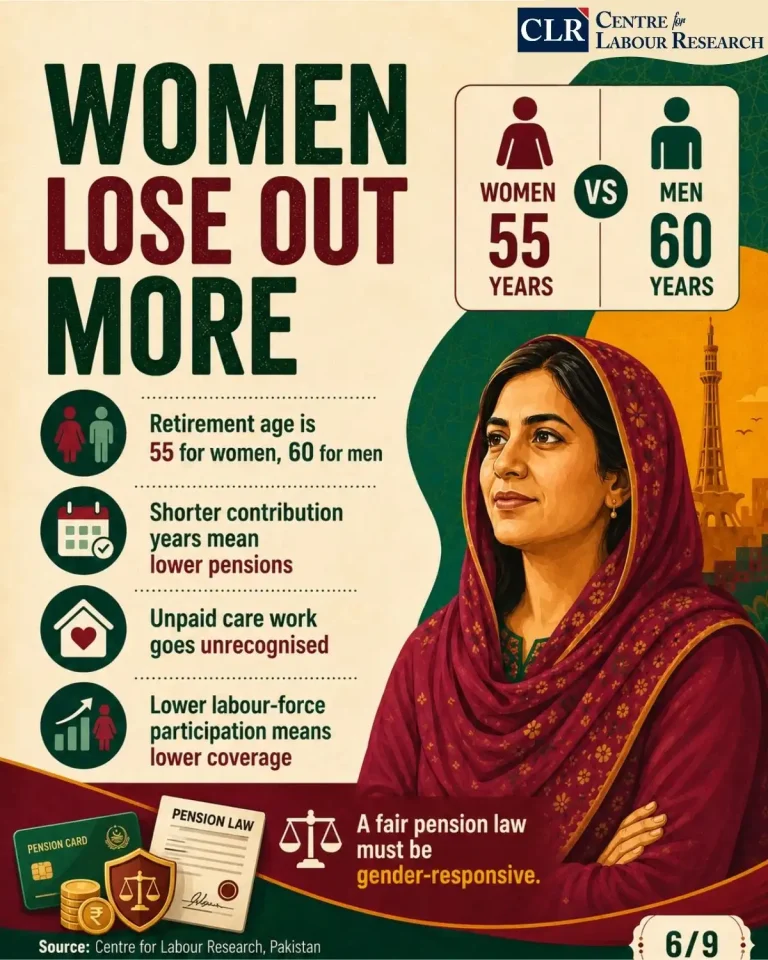

The Bill expands coverage to homemakers, especially housewives, allowing them or their families to voluntarily register themselves with EOBI and recognise their unpaid care. PBS’s 2023 Population Census counted 116.6 million women in Pakistan, including 47.5 million married women aged 15+ and nearly 4 million widowed women. The census also shows that Pakistan already has about 6.1 million women aged 60 and above.

The latest Labour Force Survey highlights the scale of this invisible contribution. In 2024–25, 67.7 million women were out of the labour force, while 66.7 million women were engaged in unpaid domestic and care work. Around 60% of women were involved in cooking, cleaning, and related household tasks, spending an average of 15.3 hours per week, while PBS also reports that 20 million women were engaged in caregiving.

These numbers expose a structural gap in Pakistan’s social protection architecture. With more than 80% of employment being informal, an old-age protection system tied primarily to formal employment will inevitably exclude a large share of women. Any serious reform must reflect the realities of women’s lives in Pakistan: early marriage, long years spent in unpaid care work, and longer life expectancy than men. Thus, it is important to first allow the voluntary registration of homemakers and housewives in the old-age benefit system.

Under current law, there is no individual pathway for workers outside standard employment, as coverage depends on being an “employee” in the formal sector. The amendment proposal creates an explicit pathway for self-employed, overseas Pakistanis, and informal workers to opt in. Moreover, it allows young workers aged 16 and above to register with EOBI and start contributing.

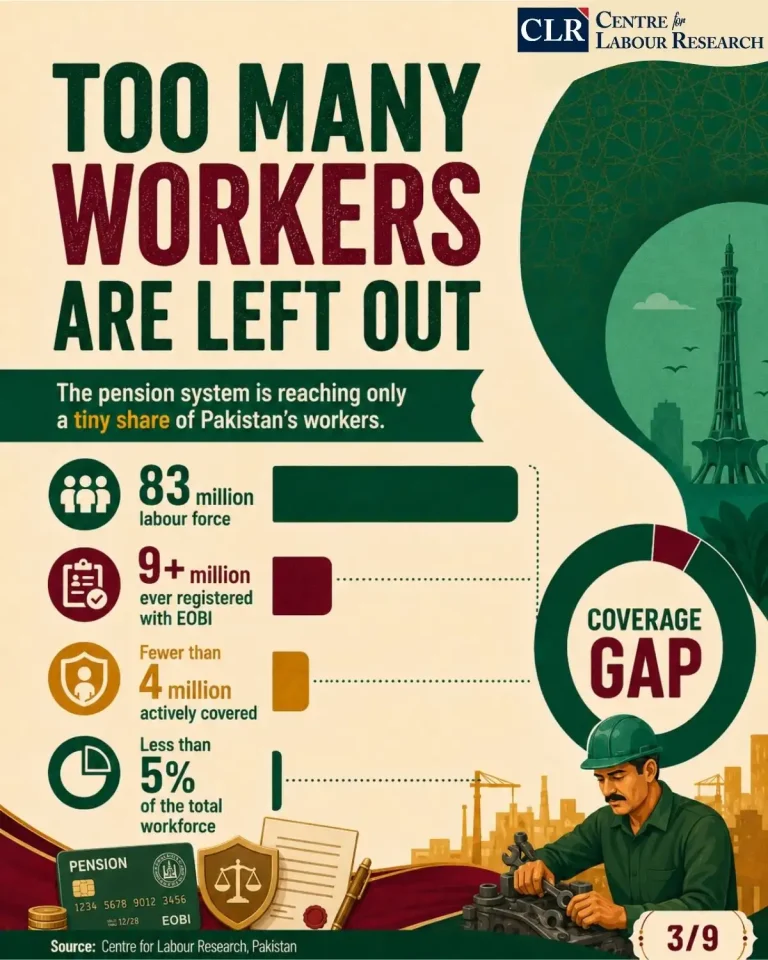

Coverage trigger for establishments: The current law applies where ten (10) or more persons are employed (and can apply to smaller units if notified. It allows voluntary registration for establishments with fewer than 10 workers. The amendment proposal drops the application to five or more workers. Enterprises may apply for voluntary registration even if they have fewer than five workers. According to the 2023 Economic Census, 95% of the 7 million economic establishments in Pakistan have fewer than 10 workers. Therefore, it is essential to expand access to the formal scheme by lowering the applicability threshold.

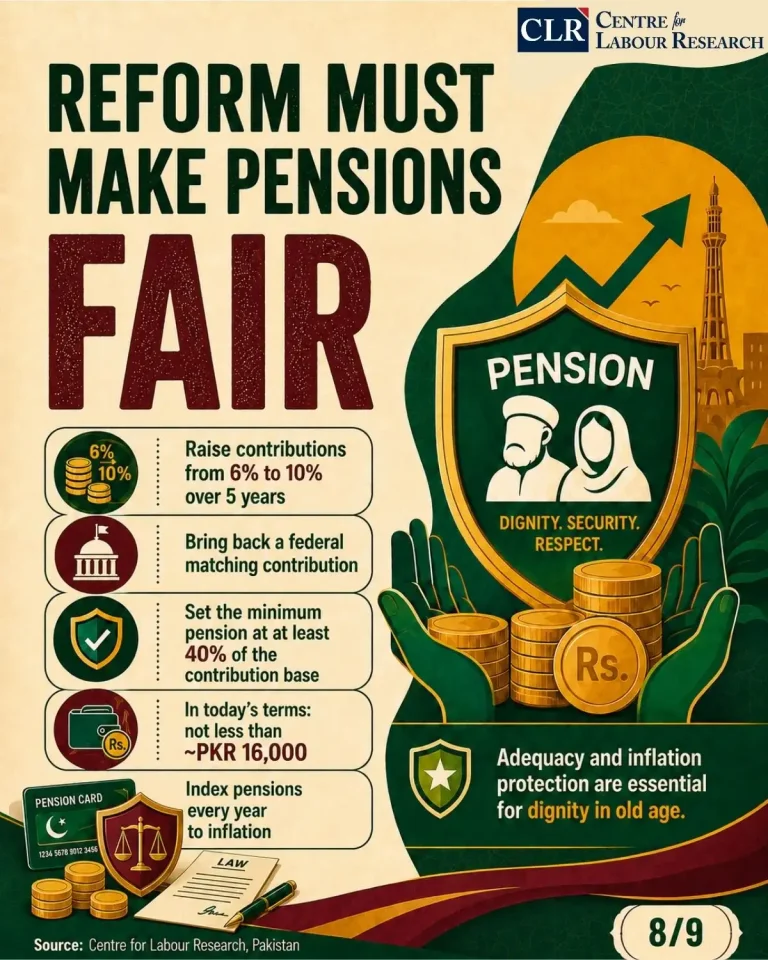

Adequate contributions and benefits: Under the current law, the basis for contributions is “wages”; the system has historically suffered from ambiguity and erosion. The amendment proposal introduces/clarifies “contribution base”, annually recommended by the Board and approved by the Federal Government and ties the floor to the minimum wage for unskilled workers (in Islamabad Capital Territory), rather than allowing contributions to collapse to very low wages, as is the case now. The reform targets benefit adequacy and reduces contribution evasion/under-declaration. Moreover, while the Government’s contribution is discretionary under the present law, the amendment proposal requires the federal government to make a matching contribution (equal to the employer’s and insured person’s contributions), as was the case before 1995. In line with international standards, contribution levels should be sufficient to ensure the system’s financial sustainability. The current contribution levels are too low, even compared to regional levels. The amendment proposal suggests a phased increase in contributions from 6% to 10% over the next five years.